The Federal Reserve just held rates steady for the third straight meeting, and if your first thought was "so mortgage rates should stay the same or finally drop," that assumption is worth examining before it shapes a major financial decision.

The Fed's April hold was not a signal of relief — it was a signal of caution, driven by elevated inflation, slower job gains, and real uncertainty around global energy prices and ongoing conflict in the Middle East. Wall Street had already priced this decision in weeks ago, which means the announcement itself moved almost nothing.

What actually moves mortgage rates — Treasury yields, inflation data, jobs reports, and geopolitical developments — is still very much in motion. For buyers, that means holding out for Fed rate cuts may not deliver the affordability break you're counting on, because mortgage rates don't wait for Fed permission to shift. For sellers, a steady rate environment carries its own set of signals about buyer motivation, pricing strategy, and timing that are worth understanding rather than ignoring.

This article cuts through the noise around Fed announcements and gives you a practical framework for what this decision actually means for your next move — whether you're trying to buy, sell, or just figure out if now is even the right time to act. The real story here isn't the hold itself, so what does the market do with everything that comes after it?

What This Means for Your Next Move Right Now

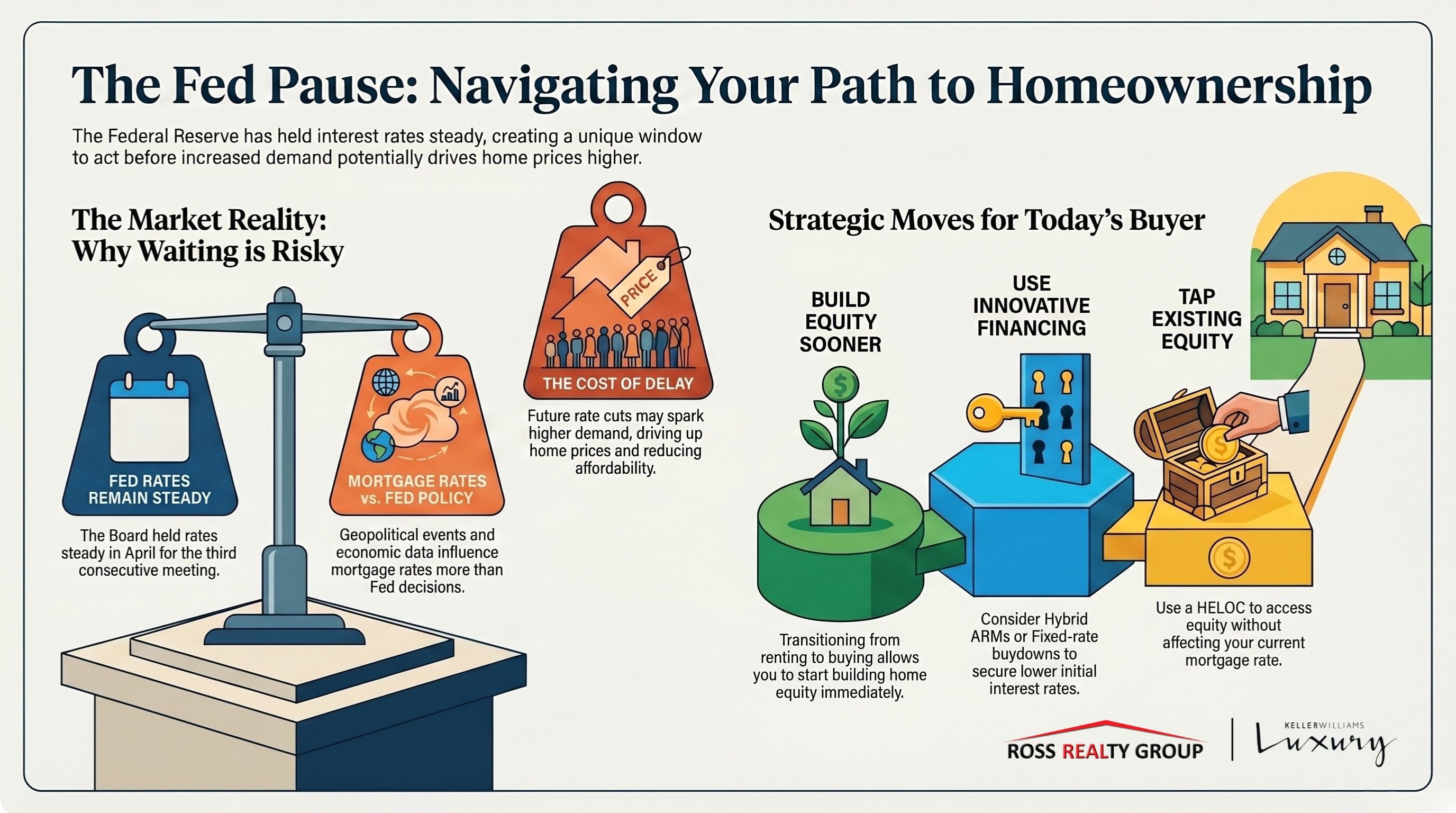

A third consecutive hold from the Fed is not a green light for lower mortgage rates — and treating it like one is a costly assumption. The Fed's decision to keep policy rates unchanged reflects ongoing caution around elevated inflation and global uncertainty, not a shift toward easier financial conditions. Mortgage rates respond to a much broader set of signals than Fed announcements alone, and waiting for the Fed to move before acting in the housing market often means waiting for something that may not deliver what you expect.

For Buyers

Bond markets and mortgage lenders had already factored this hold into their pricing well before the official announcement. That's how financial markets work — by the time a widely expected decision becomes official, the reaction has already happened. A Fed pause that surprised no one is not going to push the 30-year fixed rate down in any meaningful way. The more capable move is to work with what rates are right now, get pre-approved based on your actual numbers, and focus on what you can genuinely afford rather than a rate that may or may not materialize.

For Sellers

A rate environment that isn't moving dramatically in either direction still draws out buyers — specifically the ones who have done the math, adjusted their expectations, and are ready to act. These are not reluctant buyers hoping for a better deal next quarter. They've overcome the sticker shock of current rates and are making decisions based on real financial plans. That kind of buyer is serious, and a stable rate backdrop keeps them in the market. Pricing your home accurately and presenting it well matters far more right now than timing a sale around a Fed cut.

Bottom Line

The most empowering thing both buyers and sellers can do is stop treating Fed meetings as a decision-making trigger. Your budget, your timeline, and what's actually available in your local market are the variables you can work with. Competing listings, seasonal inventory shifts, and your own financial position will shape your outcome far more than a Fed announcement that bond traders already priced in weeks ago. Chasing perfect conditions — a lower rate, a slower market, a better moment — tends to cost more time and money than simply making a well-informed decision with the conditions in front of you.

Steady Fed policy removes one variable from the equation, which means the decisions that actually matter are the ones you make based on real data rather than rate predictions that even professional economists consistently get wrong.

Have questions about selling? Here's your answers...

Why Buyers Should Be Careful About Waiting for Rate Cuts

Many buyers operate under the assumption that a Fed rate cut translates directly into lower monthly mortgage payments — and fairly quickly. That's not how it works. The Fed controls the federal funds rate, which is what banks charge each other for overnight lending. Mortgage rates are priced off a completely different benchmark, and lenders factor in inflation expectations, credit risk, and bond market demand long before a Fed decision ever lands.

The gap between a Fed cut and any real movement in the 30-year fixed rate can stretch across months, and even then, the drop is rarely as dramatic as buyers hope. Lenders and investors have already built their expectations about future cuts into current pricing, which means a cut that's been anticipated for weeks often produces little to no movement when it finally happens.

There's also a market dynamic that rarely gets discussed in these conversations — when rates do eventually ease, more buyers come off the sidelines at the same time. That surge in demand pushes home prices up, which can quietly cancel out whatever monthly savings a slightly lower rate would have offered. A buyer who waited six months for a half-point rate improvement may find themselves bidding against more competition on a home that now costs $15,000 more than it did when they first considered it.

What's keeping mortgage rates elevated right now has less to do with the Fed and more to do with the 10-year Treasury yield, which has stayed stubbornly in the low 4% range. Mortgage rates tend to track closely with that yield, and as long as inflation remains above the Fed's 2% target and geopolitical uncertainty keeps investors cautious, the 10-year Treasury isn't going to fall sharply. That means mortgage rates are unlikely to drop significantly even if the Fed does begin cutting later this year.

Given all of that, buyers who are capable of acting now are better served by focusing on preparation rather than prediction. A few practical steps worth taking right now —

- Get preapproved — knowing your actual borrowing power based on current rates gives you a real number to work with, not a hypothetical one built around a rate that may never arrive.

- Compare loan options — adjustable-rate mortgages, buydown programs, and different loan terms can all affect your monthly payment in ways that don't depend on the Fed moving at all.

- Track weekly mortgage rate surveys — resources like the Freddie Mac Primary Mortgage Market Survey give you a reliable read on where rates are moving week to week, which is more useful than waiting on Fed meeting dates.

- Stay ready to act — when the right home comes up, hesitation is expensive in a market where well-priced inventory moves fast.

Fitting a home into your monthly budget at today's rate is the question that actually matters. A rate that might drop by a quarter point in eight months is not a financial strategy — your current income, debt load, and purchase price are.

Have questions as a Buyer? Look no further...

What Sellers Can Still Gain in a Steady Rate Market

Buyers who are actively searching right now have already done the mental work of accepting where mortgage rates stand. They're not holding out for a dramatic shift — they've run their numbers, talked to lenders, and made peace with borrowing in the mid-to-upper 6% range. That group of buyers doesn't disappear because the Fed held rates steady. If anything, a third consecutive hold removes some of the uncertainty that was making both sides hesitate.

Why Serious Buyers Are Still Active

When borrowing costs stop swinging unpredictably, buyers can plan with more confidence. A stable rate environment — even one with rates that feel high compared to a few years ago — gives committed buyers a fixed target to work with. They know what their monthly payment looks like, they know what they can qualify for, and they're capable of making a decision without waiting for conditions to improve. Those are the buyers already scheduling showings and submitting offers.

Pricing Matters More Than Waiting

Stretched affordability shifts the pressure squarely onto the asking price. When a buyer is already absorbing elevated borrowing costs on top of home prices that, according to Zillow's Home Value Index, remain positive in most metros, an overpriced listing doesn't just sit — it actively pushes qualified buyers toward better-priced competition. The sellers who are winning right now are the ones who price based on what the market will actually bear, not what they hoped to get before rates climbed.

Holding out for a rate cut to justify a higher asking price is a gamble with a weak track record. Any meaningful rate drop that materializes later will bring more sellers off the sidelines alongside more buyers, which tightens competition without necessarily improving your net outcome. Pricing competitively now, when the pool of active buyers is smaller and more focused, is a stronger position than waiting for a crowded market.

How Sellers Can Still Create Advantage

Inventory is still historically tight in many markets — a reality that keeps qualified buyers engaged even when overall sales volume is lower. Fewer available homes means a well-presented, accurately priced listing gets more attention per buyer than it would in a saturated market. Sellers who come in with a clear strategy — strong staging, professional photography, and a realistic timeline — are capable of standing out without needing rate conditions to do the heavy lifting.

Listing decisively with a well-prepared home captures buyers who are already in motion. These aren't casual browsers — they're people who have secured financing, identified their needs, and are ready to close. Waiting for a major rate shift to act means competing against every other seller who had the same idea, in a market where that influx of inventory could soften your negotiating position. Sellers who move with intention now are working with a smaller field of competition and a buyer pool that has already cleared the hardest psychological hurdle of this rate environment.

Got questions about lending? We've got you covered...

The Fed Does Not Set Mortgage Rates and That Is the Part Many People Miss

Most homebuyers assume that a Fed hold means mortgage rates hold too, and that a Fed cut means mortgage rates fall. That connection feels logical, but it's not how the system actually works. The 30-year fixed mortgage rate is not a product the Fed prices — it's a rate set by lenders responding to a completely separate set of market signals, and those signals were moving long before this week's announcement.

What the Fed actually controls is the federal funds rate — the rate banks charge each other for overnight lending. That rate has a direct and fairly predictable effect on products like credit cards, home equity lines of credit, high-yield savings accounts, and auto loans. Those products reprice quickly when the Fed moves. A 30-year mortgage is a different animal entirely, and it answers to different forces.

The main drivers behind where mortgage rates land on any given day are —

- The 10-year Treasury yield — lenders use this as their primary pricing benchmark for long-term home loans

- Inflation expectations — when investors expect inflation to stay elevated, they demand higher yields on bonds, which pushes mortgage rates up

- Bond market demand — strong demand for mortgage-backed securities pulls rates down; weak demand pushes them higher

- Investor sentiment and risk conditions — geopolitical instability, jobs data, and global economic uncertainty all shift how investors price risk, which feeds directly into mortgage pricing

With the Fed holding its policy rate in the 5.25% to 5.50% range and inflation still running above the 2% target, the bond market has little reason to price in relief. The 10-year Treasury yield — which mortgage rates track closely — has remained stubbornly elevated because investors are still absorbing the same inflation data and geopolitical uncertainty that prompted the Fed's caution in the first place. A steady federal funds rate doesn't cool those pressures. It just means the Fed isn't adding to them.

Separating Fed headlines from mortgage rate movement is genuinely useful for anyone trying to make a real estate decision right now. When a news cycle focuses on the Fed "holding steady" or "signaling cuts," that language describes interbank lending conditions — not what a lender will quote you on a purchase loan. Economist Deirdre McCloskey, examining the Fed's actual capacity to shift broader market rates, calculated the elasticity of the demand curve the Fed faces against global assets and concluded — "That's no influence." That assessment captures something important — the Fed operates in a financial system far larger than its direct reach. Knowing that distinction doesn't just reduce confusion around headlines, it gives you a more accurate framework for gauging when mortgage rates might actually shift and what economic data to watch instead of waiting on Fed meeting dates.

What the Fed Is Seeing in the Economy Right Now

The Fed's message from its April meeting is straightforward enough — "economic activity has been expanding at a solid pace," but inflation hasn't come down far enough for officials to feel confident about cutting rates anytime soon. That combination of reasonable growth and stubborn price pressures is exactly what keeps the Fed in a holding pattern rather than moving in either direction.

Growth Is Holding Up but the Job Market Is Cooling

GDP growth has remained positive, and consumer spending hasn't collapsed despite elevated borrowing costs across most loan categories. The broader economy is not flashing warning signs that would force the Fed's hand toward emergency cuts. That relative resilience actually gives policymakers the room to stay patient — there's no recession pressure demanding an urgent response.

Where the picture gets more nuanced is in hiring. "Job gains have remained low," and the unemployment rate has held around 4.4%, sitting "little changed in recent months." That's not a labor market in distress, but it's also not one generating the kind of momentum that would push the Fed toward tightening further. A workforce that's stable but not especially strong gives officials every reason to wait and watch rather than act decisively in either direction.

Inflation and Global Risks Are Keeping the Fed Defensive

The Fed raised its inflation projections, with both headline and core PCE now sitting around 2.7% — still well above the 2% target the Fed has been working toward since 2022. While inflation has dropped significantly from its 2022 peak, that last stretch back to target has proven far more resistant than many forecasters expected. At 2.7%, price pressures are not a crisis, but they're too persistent for the Fed to declare the job done and start cutting.

Adding pressure on top of that is the energy market. "Higher oil prices added a new layer of uncertainty," according to Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. A recent spike in crude prices, tied in part to "developments in the Middle East," has created fresh questions about where headline inflation goes from here. Energy costs feed directly into transportation, manufacturing, and consumer goods pricing, which means any sustained move higher in oil could slow the progress the Fed has already made. That's why officials have leaned into a data-dependent posture — committing to nothing until the incoming numbers give them a clearer path.

Holding rates steady right now is not a sign that the Fed sees calm waters ahead. The decision reflects a specific read on the data — growth that doesn't demand stimulus, a labor market that doesn't demand rescue, and inflation that doesn't yet permit relief. Each of those conditions has to shift meaningfully before the calculus changes, and none of them are moving fast enough to force the Fed's hand before more data comes in.

The Reports That Matter More Than the Fed Headline

The Fed's April statement tells you what policymakers are reacting to — but mortgage rates are already moving based on what traders expect to happen next. That forward-looking dynamic is what actually drives the rate quotes you'll see from lenders over the coming months, and it operates entirely independently of whether the Fed holds, cuts, or signals anything at all.

Current market pricing reflects an expectation that the federal funds rate stays roughly where it is through mid-2026, with only slim odds of a cut materializing later in that window. That means the Fed headline itself has very little new information left to deliver — the bigger rate-moving events will be the monthly data releases that either confirm or challenge what markets have already priced in. When incoming data surprises in either direction, mortgage rates respond, often within days.

Here are the five indicators worth tracking closely —

- Inflation reports — Monthly CPI and PCE releases are the most direct input into where mortgage rates go next. With core PCE still sitting around 2.7%, any reading that shows inflation re-accelerating would push bond yields higher and pull mortgage rates up with them.

- Job growth — Monthly nonfarm payroll numbers signal how much pressure the labor market is putting on wages and spending. Strong hiring tends to sustain inflation, which keeps rate-cut expectations pushed further out and holds mortgage rates elevated.

- Unemployment — The unemployment rate, currently around 4.4%, tells lenders and investors how much slack exists in the economy. A meaningful rise would shift expectations toward Fed cuts faster than almost any other single data point, which could pull mortgage rates lower.

- 10-year Treasury yield movement — This is the benchmark lenders use to price 30-year fixed mortgages, and it moves daily based on everything from inflation data to global risk sentiment. Watching the 10-year gives you a near real-time read on where mortgage rates are heading before lenders officially reprice their offerings.

- Major geopolitical developments — Conflict escalation in the Middle East or sudden shifts in global energy prices feed directly into inflation expectations. An oil price spike doesn't just affect gas — it runs through transportation, manufacturing, and consumer goods, which can stall the Fed's progress on inflation and keep mortgage rates from falling.

Every week brings some new headline that seems like it should change everything — a Fed official's speech, a jobs revision, a geopolitical flare-up. Most of those events move markets briefly and then fade. Buyers and sellers who react to each one end up making decisions based on noise rather than signal. Tracking this shorter list of indicators gives you a much more accurate read on where rates are genuinely headed.

Treating these five signals as a decision filter — rather than waiting on Fed meeting dates — puts your focus where it belongs. If inflation is cooling, inventory in your target area is tightening, and your monthly payment fits your budget at today's rate, those three conditions together are a stronger basis for action than any single announcement from Washington.

- Looking for a Real Estate Consultant? Find your solution here...

Final Thoughts

The Fed holding rates steady for a third straight meeting is worth paying attention to, but it is not the mortgage rate trigger many buyers and sellers are waiting for. The Fed controls its policy rate, not the rates lenders quote you on a 30-year fixed mortgage. Those move on their own based on Treasury yields, inflation data, jobs reports, and what's happening geopolitically — from energy prices to developments in the Middle East.

For buyers sitting on the sidelines waiting for rate cuts to save them money, the math doesn't always work out the way they expect. If rates do eventually drop, more buyers will likely come off the sidelines at the same time, which pushes prices up and shrinks your negotiating room. Waiting is a strategy, but it carries its own risks.

For sellers, a steady rate environment is not a dead end. Buyers who are active right now are serious. Pricing your home well and timing your listing with intention can still produce strong results, even without a dramatic rate shift in your favor.

What actually moves mortgage rates from here will be the next inflation reading, the next jobs report, and whatever happens in global markets — not the Fed press conference you already watched.

You are capable of making a sound real estate decision without waiting for perfect conditions. Talk to a lender, get current numbers, and work with what's real — not what the headlines are guessing might happen next.

Want to search for your next Home? Yes Please 😉

Check out this article next