What Is a

1031 Exchange?

The truth is... most California real estate investors are leaving tens of thousands of dollars on the table every time they sell a property.

Not because they made a bad deal. Because they didn't know about this one strategy.

A 1031 Exchange is one of the most powerful tools in real estate investing.

And this guide is going to break it all the way down — in plain English. No confusing jargon. No tax-code speak. Just the straight truth about what it is, how it works, and how to use it.

The Quick Answer

1031 Exchanges nationwide

capital gains rate in California

property — no exceptions

when exchange is done right

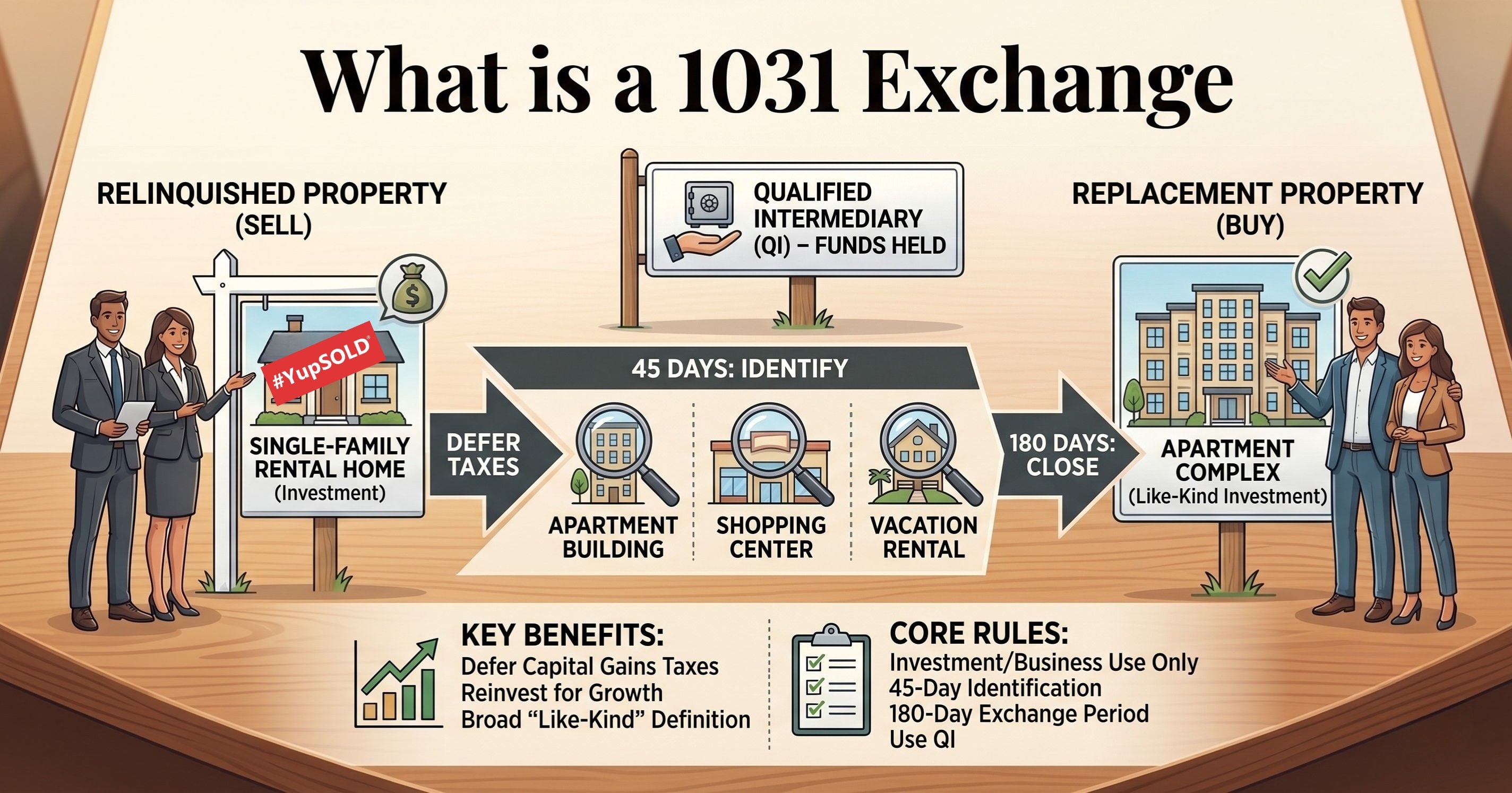

What Is a 1031 Exchange — in Plain English?

Let's say you bought a rental property in Thousand Oaks 10 years ago for $400,000. Today it's worth $900,000. That's a $500,000 gain. Nice work.

But here's the part nobody likes talking about: if you sell that property, the IRS and the state of California are going to want a big cut. We're talking potentially $150,000 to $185,000 in combined taxes — depending on your income bracket.

A 1031 Exchange (named after Section 1031 of the IRS Tax Code) lets you roll those sale proceeds directly into another investment property — and legally defer paying that capital gains tax entirely.

The tax doesn't disappear. But it doesn't come due until you sell the replacement property without doing another exchange. And here's the best part — you can keep exchanging indefinitely. Some investors use this strategy to build generational wealth over decades.

Think of it like upgrading from one level of the game to the next — keeping all your coins — instead of cashing out and handing most of them to the government every time.

🎮 The Simple Analogy

Imagine you're upgrading your car. Instead of selling your old car, paying taxes on the sale, then buying a new one with what's left — a 1031 Exchange lets you trade your old car directly for the new one. You keep ALL the value working for you, and you only deal with taxes when you eventually sell the new car outright.

💰 Without a 1031 Exchange — What California Takes

Example: Selling an investment property with $500,000 in gains

With a properly structured 1031 Exchange: $0 due at sale. Every dollar stays invested and working for you.

The 4 Hard Rules You Must Follow

The IRS doesn't negotiate on these. Miss any one of them and your exchange is disqualified — meaning you owe every dollar of capital gains tax immediately. Know these cold.

Like-Kind Property — Both In and Out

Both the property you sell (called the relinquished property) and the property you buy (the replacement property) must be real estate held for investment or business use.

Good news: "like-kind" is much broader than most people think. You can swap a single-family rental for a commercial building. A duplex for raw land. A warehouse for an apartment complex. As long as both are investment properties — you're good.

Equal or Greater Value — No Downgrading

To defer ALL your capital gains tax, your replacement property must be worth at least as much as the property you sold. You must also reinvest ALL the proceeds.

If you sell for $800,000 and only buy a $650,000 replacement property, the leftover $150,000 is called "boot" — and it's taxable. This trips up more investors than almost anything else.

The Qualified Intermediary — No Touching the Money

You CANNOT touch the sale proceeds at any point during the exchange. Not even for a day.

You must hire a Qualified Intermediary (QI) — a neutral, licensed third party — who holds the money from your sale and uses it to purchase the replacement property on your behalf. If the proceeds ever hit your bank account, the IRS considers the exchange void and the entire gain becomes taxable immediately.

Same Taxpayer — Who Sells Must Also Buy

The same person or entity that sells the relinquished property must be the buyer of the replacement property. You can't sell under your personal name and buy under an LLC — unless it's a "disregarded entity" (like a single-member LLC) that qualifies as a pass-through.

This matters a lot in California where investors often hold properties in different entities. Get advice before you structure your exchange.

The Two Deadlines That Make or Break Your Exchange

These are the deadlines that trip up even experienced investors. The IRS gives zero extensions — no exceptions for weekends, holidays, bad markets, or deals that fall through. Mark these on your calendar the moment you close.

Your Sale Closes

The clock starts the moment your relinquished property closes. Hire your Qualified Intermediary BEFORE this date. Your QI must receive the proceeds directly — not you.

Identify Replacement Property

Submit a written list of potential replacement properties to your QI. Be specific — vague descriptions invalidate the identification. You can identify up to 3 properties under the standard rule.

Close on Replacement Property

You must complete the purchase of your replacement property within 180 calendar days of your sale — OR by the due date of your tax return, whichever comes FIRST. Don't assume you get the full 180 days.

The 4 Types of 1031 Exchanges — Which One Is Yours?

Not all exchanges work the same way. The right type depends on your timeline, your market, and your goals. Here's how each one works in plain English.

Delayed (Deferred) Exchange

This is the most common type — and what most people mean when they say "1031 Exchange." You sell your property first, your QI holds the proceeds, and then you have up to 45 days to identify and 180 days to close on the replacement property.

It's called "delayed" because the purchase of the new property is delayed until after the sale. Perfect when you need time to find the right replacement.

Simultaneous Exchange

Both properties swap hands on the same day, at the same time. Think of it as a true trade. This type requires both deals to line up perfectly — same closing date, same day. It's rare, but it does happen.

Requires meticulous coordination between both parties, both escrow companies, and your QI. One delay on either side and the whole exchange falls apart.

Reverse Exchange

Here you buy the replacement property FIRST — before you sell your existing property. This is powerful in a hot, competitive market like Westlake Village or Calabasas where you don't want to miss a great deal waiting for your property to sell.

It's more complex and more expensive — your QI holds the new property in a special entity while you complete the sale — but it works when speed matters.

Improvement (Build-to-Suit) Exchange

Can't find a replacement property of equal or greater value? You can use this exchange to buy a less expensive property AND use the remaining exchange funds to build improvements on it — bringing the combined value up to equal or more than your sale price.

All improvements must be completed within the 180-day window. Your QI holds title during construction and transfers it to you when done.

What Makes California Different — Rules Every CA Investor Must Know

California is one of the highest-taxed states in the nation for capital gains — up to 13.3%. The state follows federal 1031 rules, BUT it layers on its own requirements that most out-of-state guides don't cover. If you own investment property in Simi Valley, Moorpark, or anywhere in LA or Ventura County — these rules apply to you.

The California Clawback Rule

This one surprises a lot of investors. Here's how it works: if you sell California real estate and use a 1031 Exchange to buy a replacement property in another state — say Nevada or Arizona — California does NOT let you off the hook.

The state tracks the deferred gain through its "clawback" provision. When you eventually sell that out-of-state replacement property, California will require you to file and potentially pay state taxes on the original deferred gain — even if you no longer live in California.

Form FTB 3840 — Annual Filing Required

If you sell California property and your replacement property is in another state, you must file Form FTB 3840 with your California state tax return every year until you recognize the gain or loss.

This form lets the California Franchise Tax Board keep track of deferred gains. Miss a year? The FTB can estimate your income, assess taxes with penalties, and trigger an audit. It's not optional.

Stricter QI Requirements in California

California has some of the toughest rules in the country for who can act as a Qualified Intermediary. Your QI in California must:

- Hold a bond of at least $1 million or keep your funds in a separate escrow account

- Maintain an errors & omissions insurance policy covering at least $250,000

- Act as a fiduciary under "prudent investor" standards

Related Party & 2-Year Hold Rule

Thinking about exchanging into a property owned by a family member or a related business entity? The IRS and California have increased scrutiny on these transactions in 2025.

Under the Related Party Rule, both parties must hold their respective properties for at least two full years after the exchange. If either party sells before the two-year mark, the original deferred gain becomes taxable — to both parties.

Solar Panels & Personal Property Complications

Since the Tax Cuts and Jobs Act of 2017, 1031 Exchanges are limited to real property only. Personal property — furniture, equipment, vehicles — no longer qualifies.

This gets tricky for California properties with solar panels, green energy systems, or other improvements that blur the line between real and personal property. California takes a more granular approach to valuing these items — and you may face state-level tax liability on the personal property portion that doesn't exist at the federal level.

Withholding at Close (Form 593 Exception)

California requires non-resident sellers to withhold a portion of their sale proceeds for capital gains tax — 3.33% of the gross sale price.

If you're doing a valid 1031 Exchange, you can claim an exception and avoid this withholding by filing Form 593. But this only works if you're doing a full-value exchange — not a partial one.

A Real-World Example — Thousand Oaks to LA County

Meet Maria. She's been a landlord in Ventura County for 12 years. She's ready to move up to a multi-unit property in LA County. Here's what happens with and without a 1031 Exchange.

The situation: Maria bought a rental property in Thousand Oaks in 2013 for $450,000. Today it's worth $950,000 — a $500,000 gain. She's claimed about $80,000 in depreciation over the years. She wants to sell and buy a small apartment building in the San Fernando Valley valued at $1.1 million.

❌ Without a 1031 Exchange

Maria walks away with roughly $744,500 after taxes. She can afford the new property — but at a huge cost.

✅ With a 1031 Exchange

Maria rolls the full $950K into the new property. Every dollar keeps compounding. The tax is deferred — potentially for decades or forever.

*Example is for illustrative purposes only. Tax amounts vary based on individual circumstances. Always consult a qualified CPA and tax attorney.

The 8 Biggest 1031 Exchange Mistakes California Investors Make

These aren't hypothetical. Real investors have lost hundreds of thousands of dollars making these exact mistakes. Learn them now so you don't learn them the hard way.

Missing the 45-Day Window

The most common — and most devastating — mistake. Day 46 means the entire exchange is disqualified. Start identifying replacement properties BEFORE you close your sale.

Touching the Proceeds

If the sale proceeds ever land in your personal bank account — even for one hour — the IRS considers it constructive receipt and your exchange is immediately void. Always wire directly to your QI.

Setting Up Your QI Too Late

You need a Qualified Intermediary in place BEFORE your sale closes. Not after. Not during. It cannot be added retroactively. This is the one mistake with no fix.

Identifying Replacement Properties Too Vaguely

Your identification letter to your QI must be specific and unambiguous. "A property somewhere in Los Angeles" won't cut it. Include addresses, legal descriptions, and precise details.

Buying Down in Value and Ignoring Boot

Many investors don't realize that trading down in value — or pulling out any cash — creates taxable boot. Every dollar you don't reinvest is a dollar the IRS taxes. Plan your target value carefully.

Forgetting California's Form FTB 3840

Out-of-state exchanges require annual filing of Form FTB 3840. Miss even one year and the FTB can estimate your income, assess penalties, and trigger an audit that reaches back years.

Not Having a Backup Property

What happens if your identified replacement property falls through at escrow? Without a backup property identified within your 45-day window, you have no options — and the IRS has no mercy.

Planning to Convert the Property Later

If the IRS determines you intended to convert a 1031 replacement property to personal use from the start, the transaction can be disqualified entirely. Give it time — most tax advisors recommend at least 2 years of investment use.

How to Execute a 1031 Exchange — Step by Step

Here's the exact order of operations. Follow these steps and you'll be in great shape. Skip one and you risk losing everything you worked to build.

Decide to do a 1031 Exchange BEFORE you list your property. Once your sale closes, it's too late to start the process.

Hire a Qualified Intermediary (QI) immediately. They must be in place and ready to receive funds before your closing date.

Notify escrow and your agent. Your closing documents must route proceeds directly to your QI — not to you.

Start identifying replacement properties now — ideally before your sale closes. Don't wait until Day 1 of your 45-day window.

Submit your written identification list to your QI by Day 45. Be specific. Identify at least 2–3 backup properties.

Secure financing for your replacement property. Your QI funds the purchase — but you may need additional lending to meet equal or greater value.

Close on the replacement property by Day 180. Your QI transfers the funds at closing. Title transfers directly to you (same taxpayer).

File all required tax forms — Schedule 8824 for federal, Form FTB 3840 annually if your replacement property is out of California. Work with a CPA experienced in 1031s.

1031 Exchange FAQs — Answered in Plain English

These are the questions we get most from investors in Ventura and Los Angeles County. If yours isn't here — call us. We love this stuff.

BUT — here's where the strategy gets powerful. If you keep exchanging into new properties, you can defer taxes indefinitely. And if you hold a property until death, your heirs typically receive a "stepped-up" basis at fair market value — effectively wiping out the deferred gain entirely. That's how serious real estate wealth gets built across generations.

Your primary residence doesn't qualify. Neither does a vacation home that you use personally (even if you rent it out occasionally). However, if you've converted your primary home to a full-time rental and held it as such for a reasonable period, it may qualify. Talk to a CPA about your specific situation.

Examples: a single-family rental for a commercial strip mall; a duplex for raw land; an apartment building for a warehouse; a retail store for a self-storage facility. All of these are valid like-kind exchanges — as long as both properties are held for investment or business use.

Cash boot — you sell for $800,000 but only buy a $700,000 replacement property. That $100,000 difference is boot and is immediately taxable.

Mortgage boot — if you are relieved of more debt on the relinquished property than you take on in the replacement, the difference counts as boot.

The good news: partial exchanges are fine. You just pay taxes on the boot portion while the rest remains tax-deferred.

Under the 200% Rule, you can identify more than 3 properties as long as their combined fair market value doesn't exceed 200% of your relinquished property's sale price. This is a great strategy for diversifying a large portfolio or breaking a high-value property into multiple income-producing assets.

This is why starting your replacement property search BEFORE your sale closes is so critical. And why identifying 2–3 backup properties — not just one — is always the smart move. If your first choice falls through, you still have options.

Most tax advisors recommend holding the replacement property as a legitimate investment for at least 2 years before converting it to personal use. After that, you may also be able to combine a 1031 Exchange with a Section 121 primary residence exclusion (up to $250K / $500K for couples) — but this requires careful planning and expert guidance.

Why? Because timing is everything. Your agent needs to coordinate with your QI on closing dates, understand how to structure offers on the replacement side to meet the 180-day window, and know the local market well enough to find replacement properties quickly. A great agent doesn't just find properties — they help protect your exchange.

The Ross Realty Group has helped investors across Thousand Oaks, Westlake Village, Simi Valley, Agoura Hills, and across Ventura and LA Counties navigate the 1031 Exchange process with confidence.

Stop Letting Taxes

Eat Your Equity.

The truth is... a 1031 Exchange is one of the most powerful wealth-building tools available to any real estate investor. But it requires the right team around you — a knowledgeable real estate agent, a solid Qualified Intermediary, and a CPA who knows California's unique rules.

The best part? We can help you with one third of that equation — and connect you with trusted professionals for the rest. Whether you're selling an investment property or searching for your next one — our team knows the Ventura and LA County markets inside and out.

Let's talk. No pressure. No obligation. Just honest answers.

Ross Realty Group

Serving Thousand Oaks, Westlake Village, Simi Valley, Agoura Hills, Moorpark, Camarillo, Woodland Hills, Encino, Sherman Oaks & all of Ventura and LA Counties.

Disclaimer: The information on this page is for general educational purposes only and does not constitute legal, tax, or financial advice. 1031 Exchange rules are complex and highly fact-specific. Tax laws may change. Always consult a qualified CPA, tax attorney, and licensed Qualified Intermediary before initiating a 1031 Exchange. Ross Realty Group agents are licensed real estate professionals — not attorneys or tax advisors. Ross Realty Group · Keller Williams · DRE #01938660 · agreatlistingagent.com · YupSOLD.com